|

|

|

|

October Newsletter —

We’re well into fall and approaching the end of the year. In this month's newsletter, we take a look at the state of the market, examine what mortgage data can tell us about home sales in 2026, and more. |

|

|

|

|

|

|

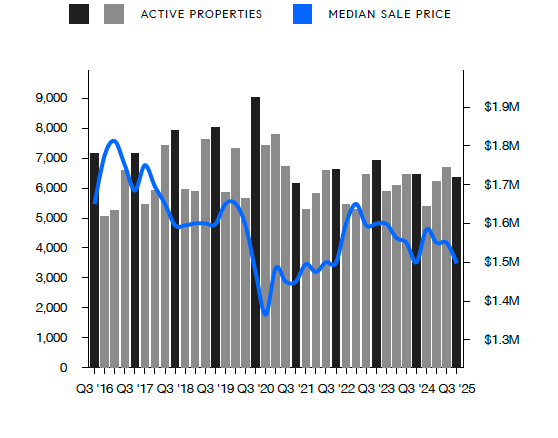

| | Despite continued economic uncertainty, New York City’s residential market showed steady resilience through the third quarter of 2025. Both Manhattan and Brooklyn posted year-over-year gains in closed sales, signaling that the recovery that began earlier in the year has largely held. Slightly lower mortgage rates and renewed buyer confidence helped fuel activity across both boroughs, particularly in the luxury sector.

In Manhattan, closed sales climbed 9% year-over-year to 2,931, driven mainly by sales priced above $3 million. Closed sales of condos and co-ops saw annual increases of 11.6% and 6.9%, respectively, while the median price rose 4.3% to $1.2 million, and the average price reached $2.02 million. Although contract activity slowed compared to Q2, it remained 4% higher than a year ago, with three-bedroom co-ops up 15.7% year-over-year as millennials and multi-generational families sought larger homes. Inventory declined slightly overall (-1.4% year-over-year), reflecting a 9.4% drop in co-op listings and a 5.7% rise in condo inventory, where the median price fell nearly 10%, creating select opportunities for buyers.

Brooklyn continued to gain momentum in Q3 with a 7.6% year-over-year increase in total sales to 2,479 closings, its highest on record for condos (+16.7% year-over-year). The average condo price hit $1.4 million, and the median reached $1.16 million, both records for the borough, while houses over $3 million surged 47% and accounted for more than 11% of all transactions. North Brooklyn led condo growth with an 11% increase in signed contracts and a 16% rise in median price, and house contracts rose 1.7% citywide despite inventory constraints. Overall inventory ticked up 1.8% from last year, but co-ops fell 24.1%, highlighting a shift toward condos and houses as buyers seek space and turn-key quality in vibrant neighborhoods.

Entering Q4, both boroughs reflect a measured optimism: buyers remain active and selective, and sellers who price appropriately continue to see strong results. Luxury transactions and record condo prices underscore New York City’s resilient appeal as the market moves through a period of gradual but steady recovery.

Let's take a closer look at the statistics from Manhattan and Brooklyn. |

|

|

|

|

|

|

| Median Recorded Sale Price |

|

|

|

|

|

|

|

|

-0.8% Quarter-Over-Quarter |

|

|

| | |

|

| | -19.6% Quarter-Over-Quarter |

|

|

| | |

|

| | | | 25.0% Properties in Contract after 180+ DOM |

|

|

|

|

| | -5.0% Quarter-Over-Quarter |

|

|

| | |

|

| | Source: Compass Q3 2025 Manhattan Market Report |

|

|

|

|

| | Median Recorded Sale Price (Quarter-Over-Quarter) |

|

|

|

|

|

| | Contracts Signed (Quarter-Over-Quarter) |

|

|

|

|

| | | | | +16.0% Properties in Contract after 180+ DOM |

|

|

|

|

| Inventory (Quarter-Over-Quarter) |

|

|

|

|

| | | Source: Compass Q3 2025 Brooklyn Market Report |

|

|

|

|

|

|

| | | After months of record-setting highs, New York City rents have finally begun to cool slightly, though they remain well above pre-pandemic levels. The citywide median asking rent in September was $3,995, up 7.2% year-over-year but down 1.4% from August, reflecting the typical seasonal slowdown that follows the summer leasing rush.

Despite the modest month-over-month dip, the rental market remains tight. Total inventory declined 6.9% year-over-year, as more renters chose to renew their leases amid a softening labor market and ongoing affordability challenges. New rental listings fell 2.5% compared to last year, further limiting options for those looking to move.

In Manhattan, inventory dropped for the 19th consecutive month, down 11.9% year-over-year, while the median asking rent climbed 7.8% to $4,600, a result of continued return-to-office demand and limited supply. In Brooklyn, the median asking rent reached $3,800, up 7% from last year, with inventory down 3.3%. Queens saw similar conditions, with rents up 6.9% to $3,207 and inventory down 3.6%.

Even as mortgage rates edge lower, purchasing remains out of reach for many. The expected monthly payment for a median-priced NYC home with a 20% down payment was $5,228 in September, still far higher than the city’s median rent and requiring an income more than double the median household earnings. With ownership costs remaining steep, renters who might have bought are opting to stay put, keeping pressure on vacancy rates and sustaining competition across boroughs.

Read the Compass September 2025 Rental Report here. |

|

|

|

|

| |

|

Deep Dive: What the Latest Mortgage Data Reveals About Home Sales in 2026 |

|

The U.S. mortgage landscape is undergoing a quiet but meaningful shift, one that could set the stage for more home sales in 2026. The average interest rate on all outstanding mortgages now sits at 4.3%, and by year’s end, that number will likely exceed pre-pandemic levels. The remarkable advantage many homeowners locked in during the pandemic, ultra-low rates below 3%, is fading as new loans originate at higher costs. |

| | This change has created what experts describe as a bifurcated market: roughly one in five homeowners enjoys rates below 3%, while another fifth faces rates above 6%. That divide is shaping behavior in ways that are likely to increase housing turnover. Homeowners with higher rates are less inclined to “hoard” their homes. Carrying costs are higher, and for many, the investment returns aren’t as strong. These owners are more likely to sell, especially if they face financial stress or job loss. After years of historically low foreclosures, we may begin to see an uptick in distressed sales in 2026, but not enough to signal a crisis.

At the same time, equity levels remain historically strong. The average loan-to-value ratio in the U.S. is 44.2%, meaning the typical homeowner has about 56% equity. Add to that the 40% of homeowners who have no mortgage at all, and it’s clear that household balance sheets are solid. Equity gains aren’t being driven solely by rising home prices. In many markets, home prices are actually lower than they were a year ago, with national averages up just 1–2% compared to October 2024. Much of today’s equity growth comes from homeowners steadily paying down their mortgages rather than from appreciation alone. |

| | That wealth has implications for the year ahead. If rates dip while unemployment rises, homeowners may tap into that equity through cash-out refinances or home equity lines of credit. This injection of liquidity could help sustain economic growth, even as other sectors cool. It also means that while foreclosures may tick up slightly, the overall risk remains contained because most homeowners have significant equity cushions.

Another key trend is the gradual unwinding of “mortgage rate lock-in.” For years, one of the biggest barriers to housing turnover was the reluctance of homeowners with 3% mortgages to trade up to homes financed at 6% or more. Mortgage “lock-in” can be measured by the gap between the average rate on existing mortgages and the current market rate for new loans; the wider the gap, the harder it is for homeowners to justify moving. Over the past three years, that gap has been narrowing. The average rate on outstanding U.S. mortgages has climbed from 3.8% to 4.3%, and by next month it’s expected to reach roughly 4.4%, matching the average from early 2020, before the pandemic housing boom began. As more homeowners take on higher-rate loans, fewer remain locked into those exceptionally cheap mortgages of the past.

If rates stay in the 6% range, the average outstanding rate will continue to rise, gradually reducing the difference between what homeowners are paying and what new buyers face. Each day, that spread narrows and fewer people are locked in.

This trend highlights that mortgage lock-in isn’t a pandemic-era phenomenon, but rather the result of long-term rate cycles stretching back through the 2010s. When market rates fall below the average outstanding rate, lock-in intensifies. When they rise above it, as they have for the past three years, the effect diminishes. In other words, higher rates are slowly curing the very lock-in they created. |

| | The irony is that the very factor that froze the housing market, high interest rates, may now be what helps thaw it. As fewer people remain locked into exceptionally low loans, we’re likely to see increased mobility, higher sales volume, and more normal turnover heading into 2026. After three years of stagnation, the balance between cheap pandemic debt and new, more expensive mortgages is evening out. The result could be a housing market that, while still expensive, finally starts to move again. |

| |

|

|

|

|

|

|

| Step into a world where Halloween Town meets Christmas Town at the New York Botanical Garden. After its sold-out debut last year, Disney Tim Burton’s The Nightmare Before Christmas Light Trail is back, bigger, brighter, and filled with new surprises. This immersive outdoor experience brings the beloved 1993 film to life with dazzling lights, festive music, and lifelike sculptures of iconic characters like Jack Skellington.

Visitors can wander through more than 8,000 square feet of glowing installations featuring interactive projections, intelligent LED lighting, and whimsical 3D-printed displays. New this year are themed refreshment and merchandise “BOOths,” offering hot cider, wine, and seasonal snacks.

The experience runs on select evenings from Thursday, September 25 through Sunday, November 30, with tickets starting at $33 for children and $45 for adults.

Click here for more information. |

|

|

|

|

|

|

|

|

| 530 East 72nd Street, Unit 4F |

| 3 BD 2 BA 1,790 SF $1,295,000 |

| At nearly 1,800 square feet, this split-layout two-bedroom home showcases direct East River views from the expansive living room, both bedrooms, and the sunroom. Highlights include a south-facing formal dining room that can easily be converted into a large third bedroom, nine closets (including two oversized walk-ins), and new floors throughout. |

|

|

| | |

|

|

|

|

| 305 East 88th Street, Unit 5G |

| 1 BD 1 BA 700 SF $599,000 |

| Located on a peaceful tree-lined block, this thoughtfully renovated home offers windows in every room, blending prewar charm with modern comfort. Original details like herringbone hardwood floors, high ceilings, moldings, and a cedar closet add warmth and character throughout. |

|

|

| | |

|

|

|

| | | 131 East 81st Street, Unit PH15 |

| 2 BD 2 BA 1,075 SF $1,495,000 |

| Welcome to PH15, a private full-floor corner penthouse in the heart of the Upper East Side. This light-filled home offers two balconies, private elevator entry, in-unit washer/dryer, a custom LEICHT kitchen, 1.5 baths, and skylights throughout, including one in the en-suite bath with heated floors. |

|

|

|

|

|

|

| 345 East 81st Street, Unit 6D |

| | Located in a prime Upper East Side location, this beautifully renovated home offers bright east-facing light and an expansive private outdoor space, perfect for morning coffee or evening entertaining. |

|

|

| | |

|

|

|

|

| 7 West 92nd Street, Unit 76 |

| | This top floor, fully renovated two-bedroom home is ideally located just steps from Central Park. With 9' ceilings, an in-unit washer/dryer, three exposures with windows in every room, and charming details like exposed brick and a decorative fireplace, this home is not to be missed. |

|

|

| | |

|

|

|

| | | | | | This newly renovated, sun-soaked home is a showstopper with stunning wraparound river and city views from southern, eastern, and northern exposures. Enjoy private outdoor space, a large eat-in kitchen, high ceilings, and an in-unit washer/dryer, all in a full-service luxury condo. |

|

|

|

|

|

|

| Fully Renovated Two-Bedroom |

| This luxurious east-facing split two-bedroom, two-and-a-half-bathroom home features oversized windows with open views, ceilings over 10 feet high, an in-unit washer/dryer, a separate office area, and central AC, all a building with more than 10,000 square feet of amenities. |

|

|

| | |

|

|

|

|

Most Recent Mortgage Rates |

| | Rates are from Citibank and are effective as of 10/27/2025. Rates are subject to change without notice. |

| Everyone’s mortgage needs are different. I have great relationships with mortgage brokers and loan officers from big banks and small banks who can help find the best loan for you. If you're looking for a lender you can trust, I'd love to help. Email me for more. |

| | | I'm an expert at successfully repositioning and selling homes that were previously listed without success. Click here for examples of how I have transformed listings to showcase a property's full potential, securing favorable deals where other agents could not. |

| Find out how Compass Concierge can help you prepare your home before coming to market by fronting the costs of upgrading, renovating, and staging at no interest. |

| I'm born and raised in New York City. If you've got a question, I've got you covered. For recommendations on anything, from where to find the best apple cider donuts to the most scenic fall day trips, it's as simple as sending me an email. |

|

|

|

|

|

|

|

|

Office: 646-982-0353 Compass is a licensed real estate broker. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions. |

|

|

|

|

|

|