| | I hope you're having a great start to Fall. After a busy end to Summer, September started off a bit quiet this year, with lower-than-expected open house traffic and a general feeling among agents that the market was slow and unfavorable to sellers. At the end of September, there was a palpable shift in the mood with on-the-ground activity up. Despite shifting perception, overall September activity (contracts signed and new listings) was up according to the released data.

Proper pricing and presentation remain key to garnering interest and offers. All of our Spring listings went into contract before the end of the Summer, and our first listing of the Fall received offers the first week it was on the market. While no one can predict how political factors may influence the market this Fall and beyond, the recent decline in mortgage rates and the influx of new buyers have us feeling optimistic for a strong end to the year.

Below are our detailed reports on the Manhattan and Brooklyn markets. Q3 data shows solid year-over-year price growth, driven by a strong Spring season. We also highlight the September data to give you a snapshot of how the Fall is going, which has so far shown continued strength. |

| | |

|

|

|

| Despite uncertainty surrounding the upcoming mayoral election, Manhattan’s real estate market showed renewed strength in Q3. The data reflects both robust Spring sales activity — since closed prices typically lag two to four months behind signed contracts — and a solid start to the Fall season.

In Q3, total closings were up compared to last year, supply remained steady, and signed contracts climbed for the sixth quarter in a row. Although total inventory for Q3 remained essentially even with 2024, as closings and contracts ticked up to offset the annual gains in new listings. Days on market also declined across all price-points this quarter, with homes priced between $500K-$1M and $2M-$3M seeing the shortest marketing times.

Prices rose across the board, due to both increased demand and strong performance in the luxury and condo markets. Interestingly, new development listings only comprised 13% of total closings — even with this time last year — indicating that the strong price performance in the luxury and condo markets was predominantly due to resales. It is important to note, however, that Q3 2024 represented a 3-year low for Manhattan price per square foot, so these Q3 figures, while above last year, still remain below peak levels. |

| |

|

|

|

| September also saw a strong influx of new listing inventory as well as 10% more contracts. Despite this strong data, Manhattan open house traffic has trended consistently below 2024 levels since June, with an extremely quiet August and appreciably lower turnout at open houses since Labor Day While some of this could be due to changes in the methodology used to collect open house data starting in early 2025, we don't have much other insight to explain the discrepancy. |

|

|

|

|

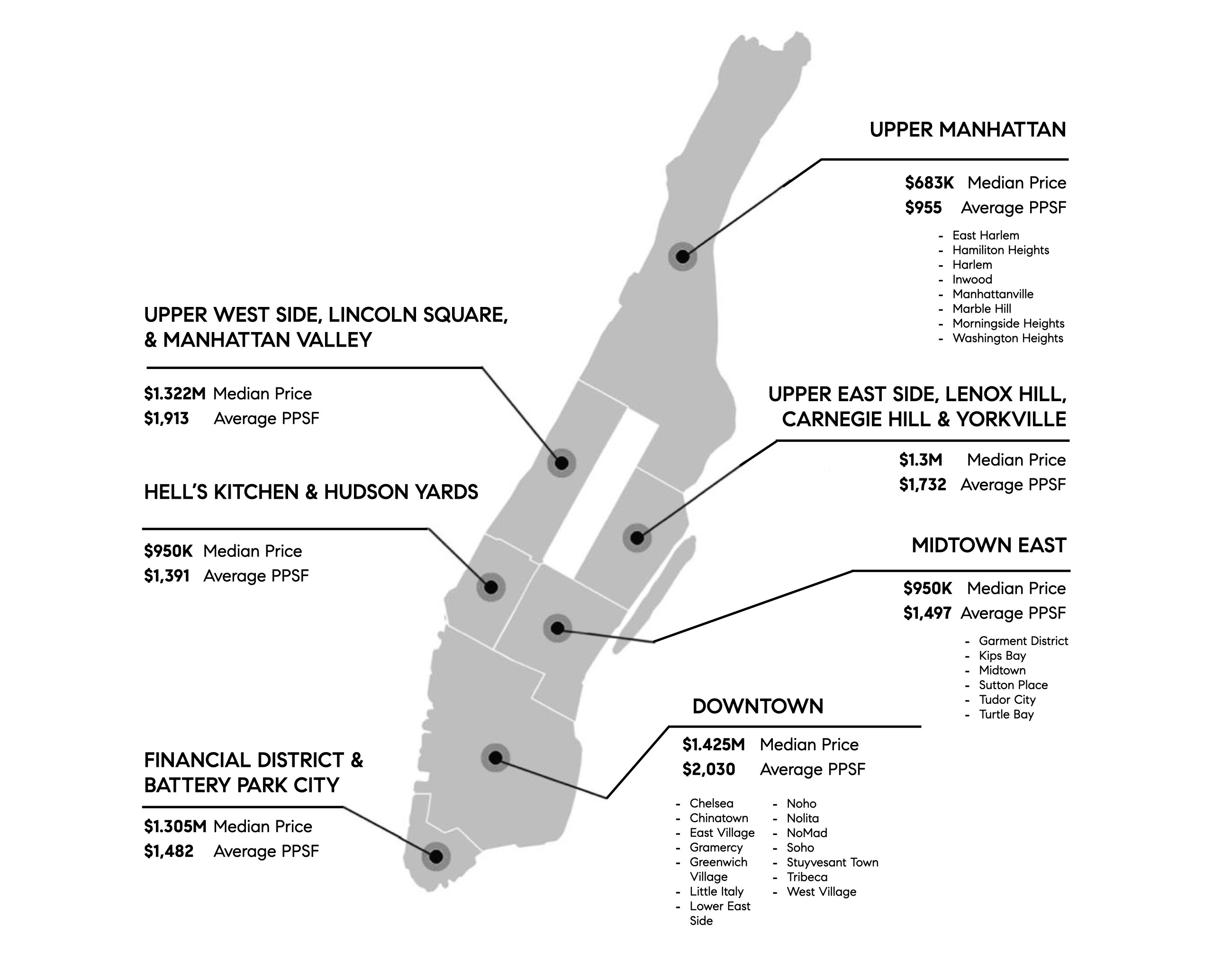

| | Looking closer at the various Manhattan submarkets, the Upper West Side, Upper East Side, and FIDI/BPC all saw strong increases in closings, contracts, and closed sale price metrics compared to last year. Downtown did not outperform 2024, with closings and average PPSF essentially even and slightly below last year and median sale prices dipped 7% due to a significant decline in new development closings in the area. While closings increased across Midtown, other indicators were mixed. Midtown West saw a drop in prices, and Midtown East saw fewer contracts signed. |

| | |

|

|

|

| In Brooklyn, we saw dismally low inventory, an increase in signed contracts, and record high prices. With fewer new development launches, and resales constrained by reluctance among sellers (who are hesitant due to the lock-in effect of their current mortgages and limited opportunities to trade up in the market), inventory was down 6% in Q3 and there were 4% fewer new listings in September, both compared to 2024. Days on market averaged 11 days fewer than last year, marking the shortest average time to contract for any quarter in the past three years.

Although the number of closings declined 2% year-over-year, total sales volume rose 11% because of higher prices. Several Brooklyn pricing indicators — median prices, average PPSF — reached record highs this quarter. Overall gains were driven primarily by new development, which saw a 38% increase in median price and a 14% increase in average price per square foot. |

|

|

|

|

| | Similar to Manhattan, despite materially better results in terms of contracts and prices, open house traffic trended below last year's levels. Again, this may be due to incomplete data collection in 2024 more than anything else. What is more interesting to note from the data is that traffic has remained relatively stable since the beginning of the Fall, rather than starting strong and showing a strong decline like last year. |

|

|

|

|

| | Every single Brooklyn submarket saw a year-over-year increase in median sale price in Q3, even South Brooklyn. Only two submarkets saw a decrease in average PPSF — Park Slope & Gowanus and BK Heights, DUMBO & Downtown BK — due to significant decreases in new development closings. Almost all submarkets saw a year-over-year decline in total closings. The exceptions were Williamsburg and Greenpoint, which rose 16% thanks to increased new development closings in South Williamsburg, and Boerum Hill & Carroll Gardens, which jumped 75% versus last year—driven largely by Bergen Brooklyn, a 105-unit new building that began closings In Q3. |

| |

|

|

|

| | | With the government shutdown, the latest Jobs Report which had been set for October 3 has been put on hold, and there is no clear answer as to when or if the report will be released at all. While private reports suggest there has been further deterioration, without the official report, it’s much harder to predict the likelihood of the Federal Reserve cutting rates later this month and/or when they meet in December. Forecasts are inconsistent, but mortgage rates have been slowly declining. Currently, fixed loans are hovering right around 6% with 7-year adjustable rate loans inching closer to 5%... |

|

|

|

|

| | RATE DATA BASED ON BASED ON CITIBANK'S 30-YEAR FIXED-RATE FOR NON-CONFORMING LOANS, COURTESY OF ZACK TOLMIE, SR. LOAN OFFICER. |

| | | According to the Miller Samuel report, Manhattan’s co-op and condo market hit a two-year high in Q3 2025, with signed deals up 11% year-over-year. Inventory remains tight, down 15% from last year, driving competition and quicker closings. Notably, the median sale price for condos rose 6.5% to $1.2M, while co-op prices remained stable. (BRICKUNDERGROUND)

Manhattan's luxury housing market is experiencing a remarkable surge, defying national trends. In Q3 2025, luxury home sales in the city rose 13.6%, with a median price surpassing $5.9M. Notably, 90% of transactions over $3M were cash deals, underscoring strong demand despite mortgage rate fluctuations. (NY POST)

Bloomberg’s new analysis finds that nearly one in three New York City renter households earning over $100,000 are now considered rent-burdened, spending more than 30% of their income on housing. Median rent in the city has climbed to about $3,700, up roughly 35% since 2019, with some neighborhoods seeing increases of 50–60%. (BLOOMBERG)

Manhattan rents held steady in September, with the median price for a brokered apartment at $4,550—just under August’s figure but still about 8% higher than a year ago. Although some of the factors that drove rents higher have begun to ease, prices aren’t expected to decline significantly in the near term—barring a broader economic downturn—as many would-be buyers are staying in the rental market due to interest rates. (THEREALDEAL)

Across the country, some once-hot markets in the Sun Belt, like Austin and Tampa, are starting to shift in favor of buyers as inventory rises and demand cools. New York City and much of the Northeast, however, remain strong seller markets with tight inventory is tight and steady buyer interest. (THEREALDEAL) |

| | | Explore a curated collection where cozy fall vibes meet timeless townhome living. |

| | |

|

|

|

| | | | | | | | "Isil and her team were exceptionally helpful in our search for a home in Brooklyn. They were diligent, proactive, and helpful at every step of the process--from highlighting interesting listings, to arranging walk-throughs and gathering information, to the bidding process itself. She made sure the whole process was fun, efficient, and, most importantly, successful! We would love to work with her and her team again."

- Buyers of a Fort Greene Townhouse |

|

|

|

|

| | Office: 646-982-0353 Compass is a licensed real estate broker. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions. |

|

|

|

|

|

|