| | We hope you had a restful holiday season and are enjoying a smooth start to the new year. We’re pleased to share our Q4 market recap below.

The second half of 2025 was a balanced market. Buyer demand was strong but sensible, and sellers who priced reasonably or offered a more in-demand product achieved excellent results. We saw this firsthand, with several best-in-building sales on our listings and competitive bidding with our buyers, underscoring the importance of strategic pricing and presentation.

Activity picked up meaningfully toward year-end, with closings outperforming both 2023 and 2024 and coming in stronger than many expected. That performance reinforces a theme we’ve returned to throughout the year: demand is there, but buyers are more selective.

Manhattan prices were generally stable across the board, with the luxury sector standing out as a particular area of strength. After a softer spring in Brooklyn, persistent inventory constraints, particularly in the most in-demand neighborhoods, continued to put upward pressure on prices.

As we head into 2026, we’re busy preparing listings for the spring market and working closely with buyers as they wait for new inventory to come online. If you’re considering a real estate move this year, now is an ideal time to lay the groundwork, and we’d be happy to connect.

Stay warm this weekend -- it's going to be a doozy! |

| | |

|

|

|

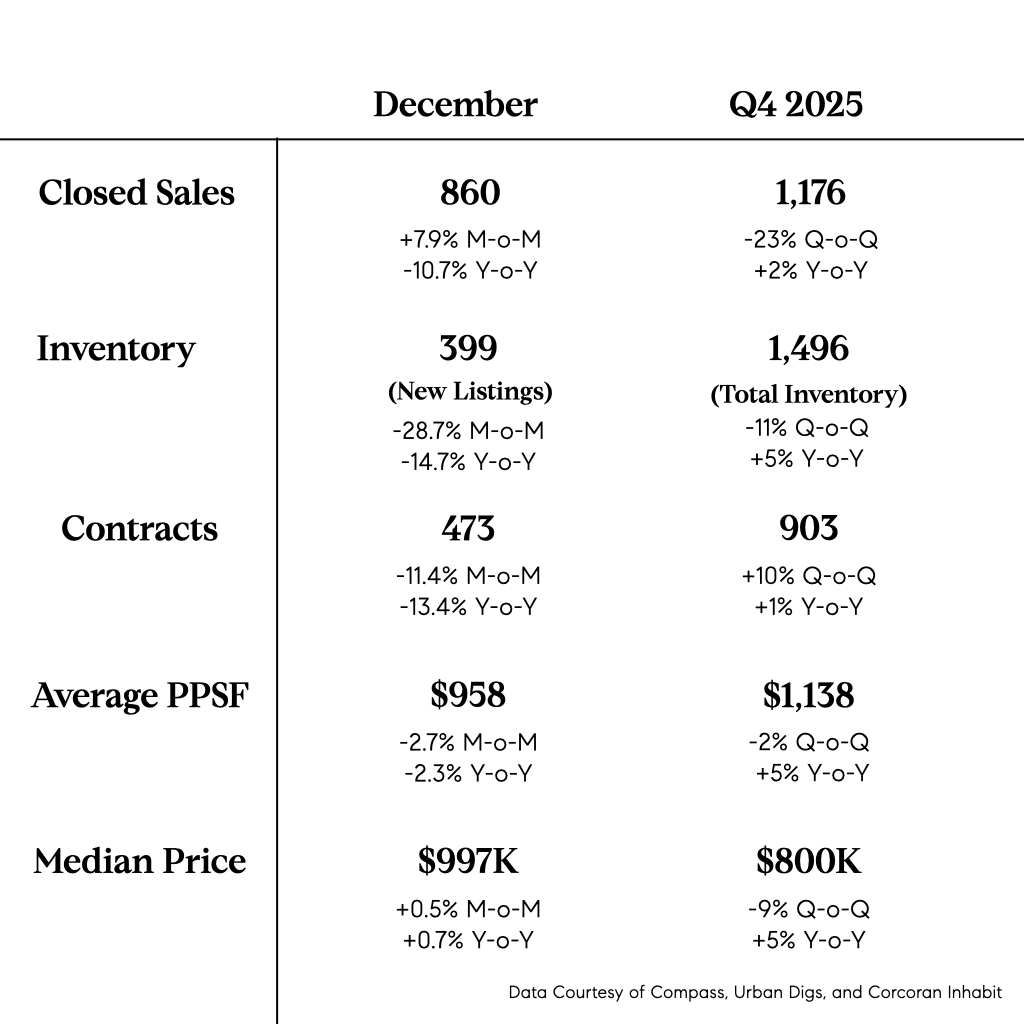

| Despite no meaningful shift in interest rates, a contentious mayoral election, and constant headlines about economic and political uncertainties, buyer demand in Manhattan was strong throughout the second half of 2025. After two challenging years, the market was solidly "neutral" and outperforming 2023-24 across essentially all meaningful metrics: Q4 closings were up 8.6% and contracts were up 5%, year-over-year, building strong momentum going into 2026. Despite fewer new development listings, inventory ticked up slightly, driven by a surge in resales.

Prices were resilient in Q4 with notable gains in luxury condo sales, which reached an all-time average high while coops posted their second highest fourth-quarter closed sale prices on record. Closed sale price per square foot ticked down slightly, although this was primarily due to a decrease in ultra-luxury new development closings. |

| |

|

|

|

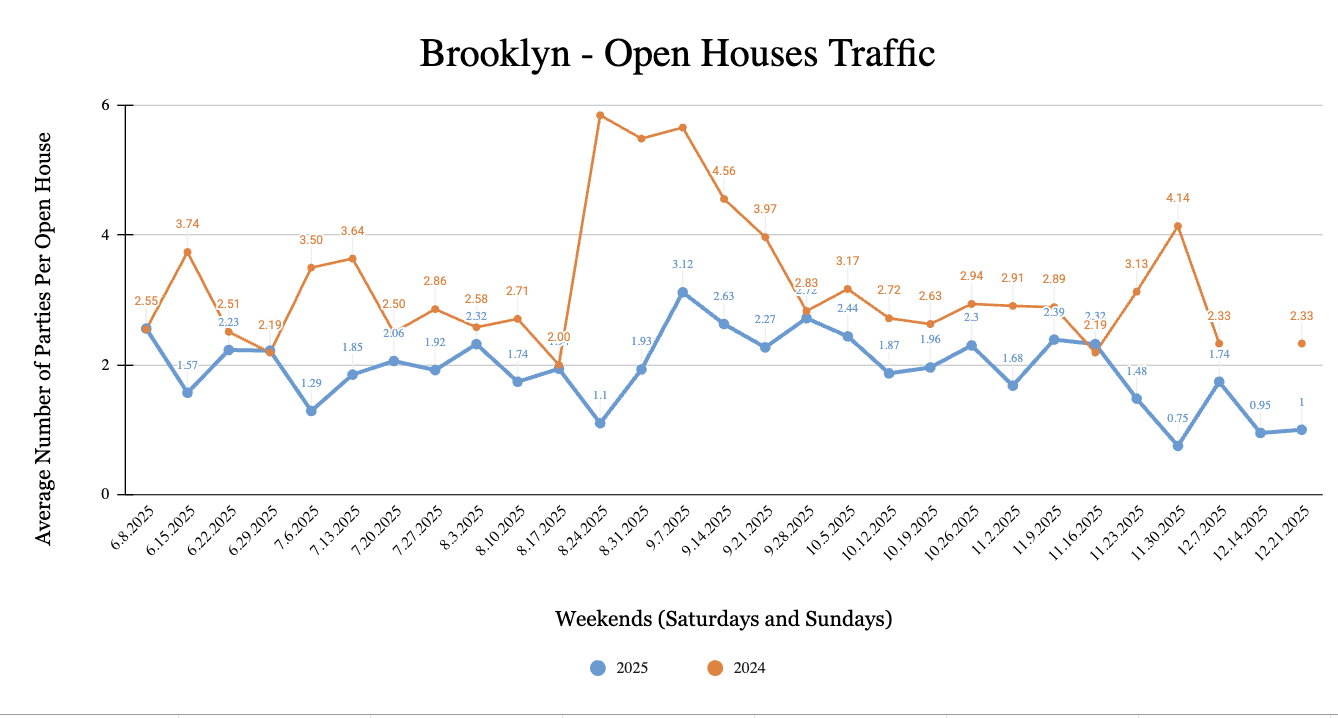

| Despite stronger market indicators, Compass reported lower open house traffic in Q4 compared to 2024. Some of this discrepancy may reflect meaningful shifts in buyer behavior, although most is likely attributable to changes in data collection adopted in early 2025. Beyond methodology, the decline may also reflect increased reliance on private appointments rather than traditional weekend open houses.

More instructive, however, is the comparison within 2025 itself. Fall open house traffic generally outperformed spring levels using the same methodology, pointing to stronger buyer engagement in the second half of the year, consistent with the broader narrative of momentum building throughout 2025. |

|

|

|

|

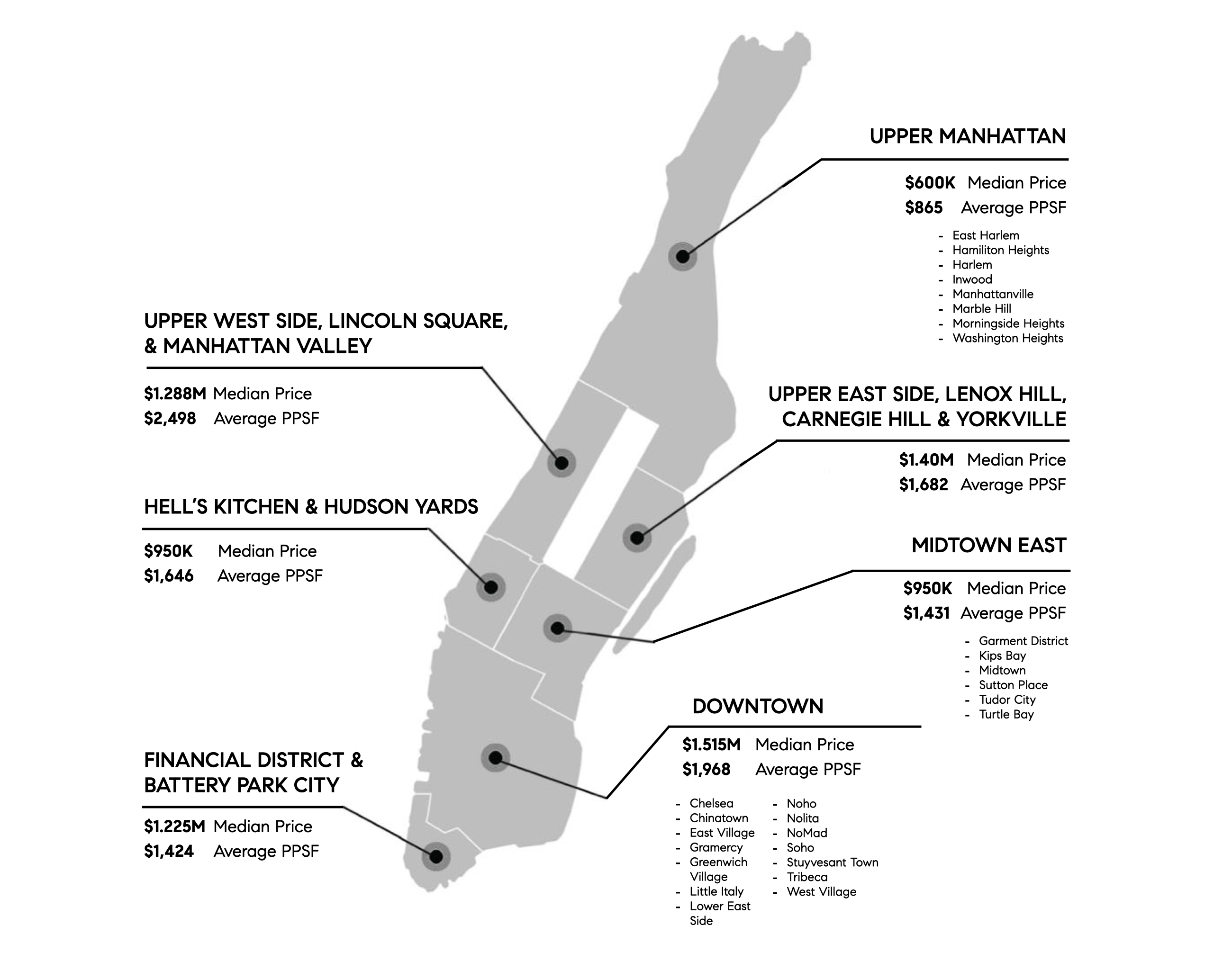

| | Looking across the map, the Upper East and Upper West Sides showed strong growth in Q4 with an increase in inventory, closings, and median sale prices, and a decrease in days on market.

On the other end of the spectrum (and map), a 30% decline in new development closings drove a pull-back in Downtown activity, with total closings falling for the first time in five quarters. This shift also translated into lower pricing, with average price per square foot declining 15% year-over-year.

In Midtown, closings fell though prices remained relatively stable. |

| | |

|

|

|

| As we've come to expect, the Brooklyn market in Q4 was once again plagued by low inventory. While on paper new listings were up 5% compared to Q4 2024, they were still 18% below the ten-year fourth-quarter average, and were heavily concentrated in the first few weeks of the fall market. New development inventory, which has buoyed overall Brooklyn inventory over the past few years, was down 15%, hitting a ten-year fourth-quarter low.

Somehow, even in this challenging inventory environment, overall buyer demand in Brooklyn held strong - both signed contracts and closings ticked up modestly. This translated to near record-high prices for the borough.

The trend toward larger and more expensive properties continued, driven by their limited supply in the most in-demand neighborhoods and the relatively muted impact of higher mortgage rates on these buyers compared to those at lower price points. Differences in days on market across these property types is illustrative: 1-bedroom and studio listings both saw significant increases in days on market compared to Q4 of last year, while 2-bedroom marketing times remained essentially even, and 3+ bedroom homes were on the market 12% fewer days. Correct and strategic pricing, especially in the lower (<$1M) sector of the market, remains key. |

|

|

|

|

| | Consistent with Compass’s reported Manhattan open house data, traffic in Brooklyn trailed the 2024 levels. As noted above, a significant portion of this difference reflects changes in reporting methodology, resulting in a larger and more comprehensive data set.

Looking within the quarter, however, the more meaningful shift occurred late in November and into December, attributable to the sharp decline in new listing inventory toward year-end, rather than a signal of waning buyer demand. |

|

|

|

|

| | Price per square foot was up across the borough, except in Williamsburg & Greenpoint (coming off an all-time high in Q4 2024) and Bed-Stuy, Crown Heights & PLG; these areas saw fewer new development listings and closings, and fewer sales over $1M.

Park Slope & Gowanus showed the strongest performance, with total number of sales climbing 60% year-over-year, driven by growth across all product types, most notably an almost two-fold increase in new development closings. It also had the shortest average marketing time, and closed sale figures rose.

Declines in new development drove down closings in the areas of Fort Greene, Clinton Hill, & Prospect Heights and Carroll Gardens, Boerum Hill, & Red Hook. South Brooklyn also saw a 5% decline in closings, and a 2% drop in overall marketshare, likely due to greater price and rate sensitivity from buyers in the lowest price tiers of the market. |

| |

|

|

|

| | | Since early October, mortgage rates have remained relatively steady in the low-6% range. The widely-anticipated December rate cut had little impact on day-to-day pricing. Ongoing delays and gaps in economic reporting tied to the shutdown contributed to this stability, as lenders had limited visibility to proactively reprice risk.

Since the new year, political developments (Greenland, Venezuela, investigation of the Fed) that might normally have pushed rates higher have been largely offset by resilient economic data and Fannie Mae’s plan to purchase roughly $200B of mortgage bonds. Right now, all eyes are on who will succeed Powell as Fed Chair when his term ends in May, as that decision could shift expectations for 2026, which currently include just one anticipated rate cut.

Against that backdrop, one notable shift in Q4 has been the changing relationship between conforming and jumbo (>$832,751) loan rates. For years, jumbo loans often carried rates roughly 1% lower than conforming loans, which in some cases encouraged buyers to put down less than they otherwise might have in order to access the lower rate. Since mid-2024, the two have been nearly identical, and by Q4 the relationship inverted: conforming rates have consistently priced about 0.25%–0.375% below jumbo rates (at least at Citibank and other major banks we track closely). This marks a meaningful shift, making larger down payments more impactful than they’ve been in years. |

|

|

|

|

| | RATE DATA BASED ON BASED ON CITIBANK'S 30-YEAR FIXED-RATE FOR NON-CONFORMING LOANS, COURTESY OF ZACK TOLMIE, SR. LOAN OFFICER. |

| | | Manhattan real estate continues to favor cash buyers. In 2025, 64% of Manhattan condo and co-op sales were all-cash transactions, the highest share on record — up from 61% in 2024. For properties priced above $3M, nearly 90% sold without financing, highlighting how liquidity is shaping competitive dynamics in today’s market. Meanwhile, median prices climbed and high-end sales above $4M grew more than twice as fast as other segments. (NYTIMES)

NYC housing in 2026 looks competitive, especially at the top end. Brokers note that luxury and well-priced listings are seeing strong demand, with crowded showings and quick contracts in neighborhoods like Park Slope, Cobble Hill, and Brooklyn Heights. Buyers relying on mortgages may face pressure as all-cash and affluent buyers dominate many segments. (CURBED)

City Council passes new co-op admissions timing bill. Starting in 2026, co-op boards in buildings with 10+ units will have strict deadlines to acknowledge and respond to purchaser applications, helping reduce delays in closings and financing. Other proposed co-op reforms, like disclosure requirements or explanations for rejections, did not pass. (HABITAT)

In 2025, NYC new development slowed, with contract signings down roughly 11% year-over-year across Manhattan and Brooklyn. The slowdown was driven less by demand and more by shrinking inventory, as new development listings fell in both boroughs. Buyers remained selective, with well-priced, well-located projects continuing to perform. (THEREALDEAL)

New York City’s housing growth is struggling to keep pace with demand. Even with tens of thousands of new units added since early 2024, long construction timelines, regulatory hurdles, and high costs continue to slow overall development, keeping the market competitive across neighborhoods. (NYTIMES) |

| | | Explore a curated collection of NYC apartments featuring amenities that go above and beyond.

|

| | |

|

|

|

| | | | | | | | “Isil and her team helped us with what would have been a rather stressful and difficult sale had it not been for her help. She guided us from start to finish with the listing process and was very dedicated and professional, and had amazing finishing touches for the apartment and the listing. She also handled a lot of the behind the scenes wrangling for us and had contacts with all the other necessary players in the process such as lawyers, movers, and contractors, which further helped. All in all a 10/10 A+ experience with an outstanding and excellent broker.”

- Jorge, Seller of a Co-op in Chelsea |

|

|

|

|

| | Office: 646-982-0353 Compass is a licensed real estate broker. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions. |

|

|

|

|

|

|