January 2023 Market Update |

The 2023 market is already showing signs of promise after a sluggish second half of 2022. Many are speculating that the worst is behind us in light of the following national metrics: 1. There was a 25% increase in weekly mortgage applications three weeks ago, and an additional 7% increase last week. 2. Mortgage rates are at a 4-month low and are expected to hold steady or decrease. 3. There’s an increase in buyer interest, open house traffic, and offers.

4. Pending closings were down 30+% at points in the Fall, but over the last few weeks pending listings in most major markets are flat year-over-year. 5. Home builder sentiment improved for the first time in a year.

These trends largely track in NYC. Top NYC mortgage officers we have spoken to have seen a dramatic uptick in prospective buyers seeking or renewing their pre-approval letters since early- to mid-January. Rates are now at a 4-month low (about one percent or 100 basis points below October levels) and lenders believe this is only the beginning of improving rates. This sentiment was further buoyed by Wednesday's announcement by the Fed of a modest 1/4 point rate increase with a "couple more" expected in coming months. The stock market and 10-year Treasury rate responded positively, and some banks cut their rates almost immediately (for example, Citibank by 1/8 percent). The jobs report added a bit of a wrinkle, coming in much stronger than expected with over half a million new jobs added to the economy. Generally, concerns over rising unemployment serve as the main brakes on the Fed raising rates to control inflation, so this seemingly leaves the Fed open to more rate hikes. But at this point the lending industry seems to be focused on what the report said about wage growth, which remained stable, supporting the Fed’s interpretation that the US has entered a period of disinflation. While it is impossible to say for sure what the Fed will or will not do, there is some confidence that inflation was transitory and has gotten under control, easing the pressure on the Fed to raise rates, which likely means stable to decreasing rates over time.

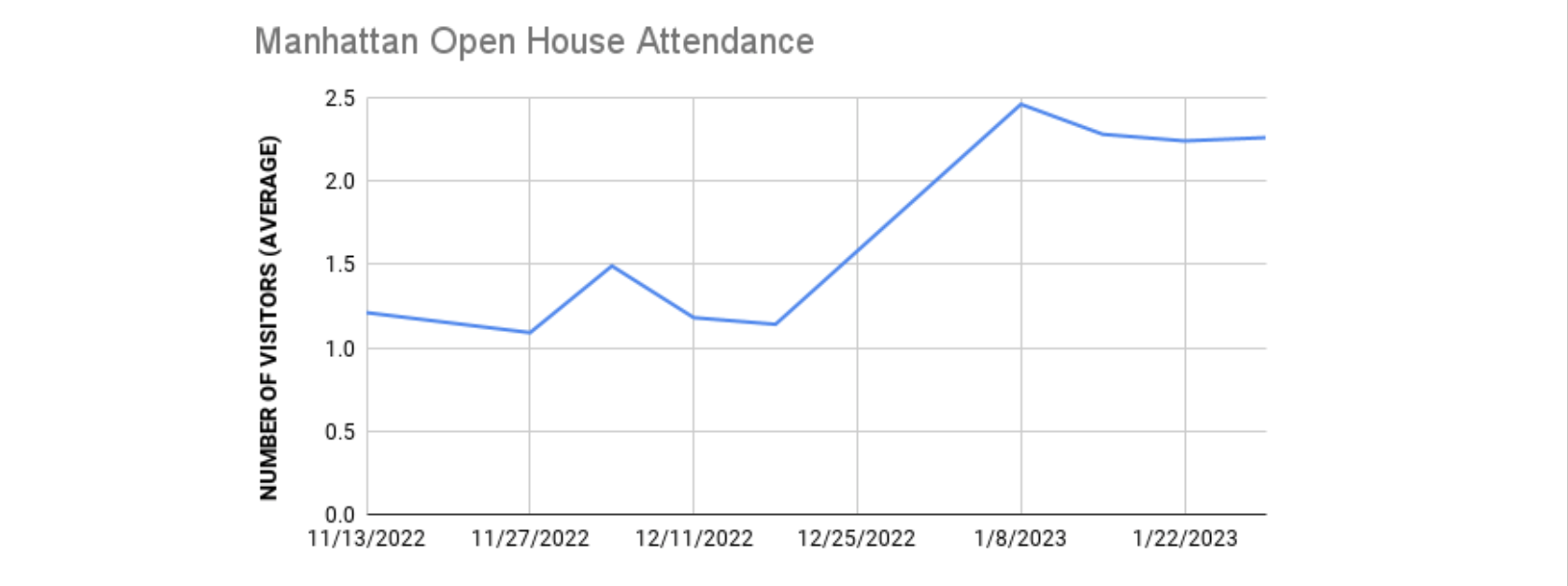

Since the start of the new year, NYC has also seen a notable uptick in buyer activity. In addition to increased mortgage applications, open house attendance is up markedly. Compass agent open house surveys throughout November and December showed Manhattan open houses receiving 1.09-1.51 buyers on average, with more than 35% getting zero visitors. Since the start of the new year average weekly attendance has ticked up to 2.24-2.46 visitors, and the percent of open houses with zero visitors has dropped below 15% for the last three weekends. Brown Harris Stevens' open house survey reports similar results with average Manhattan visitors at 2.03-2.53 visitors weekly on average since January 18 versus 0.96-1.21 in October and November.

|

Pending sales -- or "in contract" listings in NYC parlance -- have not recovered in NYC to the same extent as in other markets, on paper. In Manhattan, versus many other markets, it takes on 7-20 days from the time an offer is accepted for a contract to be signed. Due diligence often takes up the lion's share of this time, and is not a factor in many other markets. Given this lengthy time to contract, we wouldn't expect January activity to be fully reflected in January contract figures but would expect a bump in February. |

Closed sale prices were down in January reflecting market volatility caused by lower transaction volume. As we noted in our Fall newsletters, inventory was way down in the Fall as many sellers opted to wait out what was viewed as a blip in the market. While special properties traded at or above what they would have in a strong market, other properties did not fare as well bringing down overall metrics. However, it is important to note that we are talking about a small number of "deals" on these properties, versus historical prior downturns where supply remained high causing widespread contraction in prices.

Continuing a trend we saw throughout the end of 2022, Manhattan new inventory remained below historical averages in January, as some sellers still seemed wary to enter the market, though this might change as January trends become publicized. Based on rates, inventory levels, open house traffic, and our experience on the ground, we anticipate February to reflect more clearly the positive trends in the market. |

As we’ve come to expect, Brooklyn was overall less affected by rising rates in the Fall, and since the start of the new year has seen an even faster uptick in activity than Manhattan. In addition to significantly higher open house traffic - 4+ visitors on average based on all Compass agent open house surveys since the start of the year - January contract activity, while nowhere near the manic levels we saw in January 2021 and 2022, were slightly higher than in January 2020, indicating Brooklyn market activity is still in line with pre-pandemic norms. |

Inventory in Brooklyn remains constrained, especially in certain areas, with ~31% fewer new listings entering the market this January than last. January closed sale price metrics in Brooklyn all saw year-over-year increases, unlike in Manhattan, indicating that while fewer deals were done in the final quarter of 2022, prices in Brooklyn have not softened. As rates continue to improve we expect buyer demand to increase, with fast paced absorption and multiple offers on certain property types remaining hallmarks of the Brooklyn market in 2023. |

The Fed unanimously approved a quarter-point interest rate hike on Wednesday, slowing the pace of its increases in a clear sign that the central bank is seeing progress in its battle with inflation. The decision comes after months of jumbo-sized rate increases intended to cool the economy, and marks the return to a more traditional interest-rate policy. |

Gov. Kathy Hochul proposed extending the 2022 construction deadline for New York City projects grandfathered under the now-expired 421a program, giving developers until 2030 to finish their projects and still receive the lucrative tax break. (REAL DEAL) |

"Days on market" -- the number of days, weeks, months, or even years a listing has been for sale -- is not a straightforward metric and its effect on pricing and negotiations is more nuanced than one might think. |

With mortgage rates at their lowest point since September, mortgage application volume jumped nearly 28% compared the week of January 18. |

Want to indulge in some real estate fantasies and see how the ultra rich live? Check out Compass's Ultra Luxury Report. |

With all the noise about the housing market nationally and locally, it is important to note that real estate -- especially in NYC -- is hyper local. Every neighborhood, block, even building, is impacted differently by macroeconomic conditions, and the market can differ wildly for specific price points or property types. While we hope you find these reports helpful in discerning trends in NYC, they may not reflect how your property might perform or what to expect from your home search. If you have questions, we are always here to provide a consultation.

|

Make sure to take a peek at our current and upcoming listings below. We’ll be back next month with more real estate news. Until next time! |

|

© Compass 2023 ¦ All Rights Reserved by Compass ¦ Made in NYC

Compass is a licensed real estate broker. All material is intended for informational

purposes only and is compiled from sources deemed reliable but is subject to

errors, omissions, changes in price, condition, sale, or withdrawal without

notice. No statement is made as to the accuracy of any description or measurements

(including square footage). This is not intended to solicit property already listed.

No financial or legal advice provided. Equal Housing Opportunity.

All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS.

Photos may be virtually staged or digitally enhanced and may not reflect

actual property conditions.

marketingcenter-newyorkcity-manhattan

|

|

|