With another year behind us, we would like to take a moment to thank all of our clients, colleagues, and friends for your trust and continued support in our business. 2022 was a very special year for my family as we welcomed Cecilia Jeanne Dobie (Cece) in August. She’s growing like a weed, and her older brother Teddy (now almost 4) is absolutely obsessed with her. We'll be back in your inbox in early February to report on the start of the 2023 market. In the meantime, we wish you and your loved ones a wonderful holiday season and a healthy and prosperous new year! |

The end of the Fall season saw more of the same in Manhattan: decreased contract activity but prices (and other market metrics like days on market, and negotiability) largely held up due to ever-tightening inventory.

While 699 contracts signed in November -- representing an almost 50% drop year-over-year -- seems stunning, it does not tell the whole story. 2021 was an anomaly in terms of contract activity with a whopping 1,315 contracts signed in November. But over the last 10 years, we would expect 800-900 contracts in a typical November. On the supply side, active inventory continued to decline. Inventory in mid-December had shrunk by 19% in two weeks, and represented 29% fewer available listings compared to 2021 for the same time period. With the holidays approaching, we expect inventory to contract even further through most of January with many sellers delisting in the face of waning buyer activity (fewer showings, traffic in addition to contracts signed). A Compass-wide survey of Manhattan listings indicated that of the 270 open houses hosted thus far in December, 92 (~34%) had zero visitors.

While days on market is up slightly from October, low inventory has thus far buoyed prices with November closed sales prices slightly higher than both this October and last November. Although we expect inventory to remain low for some time, we will likely see price reductions and conservative pricing from sellers who cannot wait out the current financial situation. |

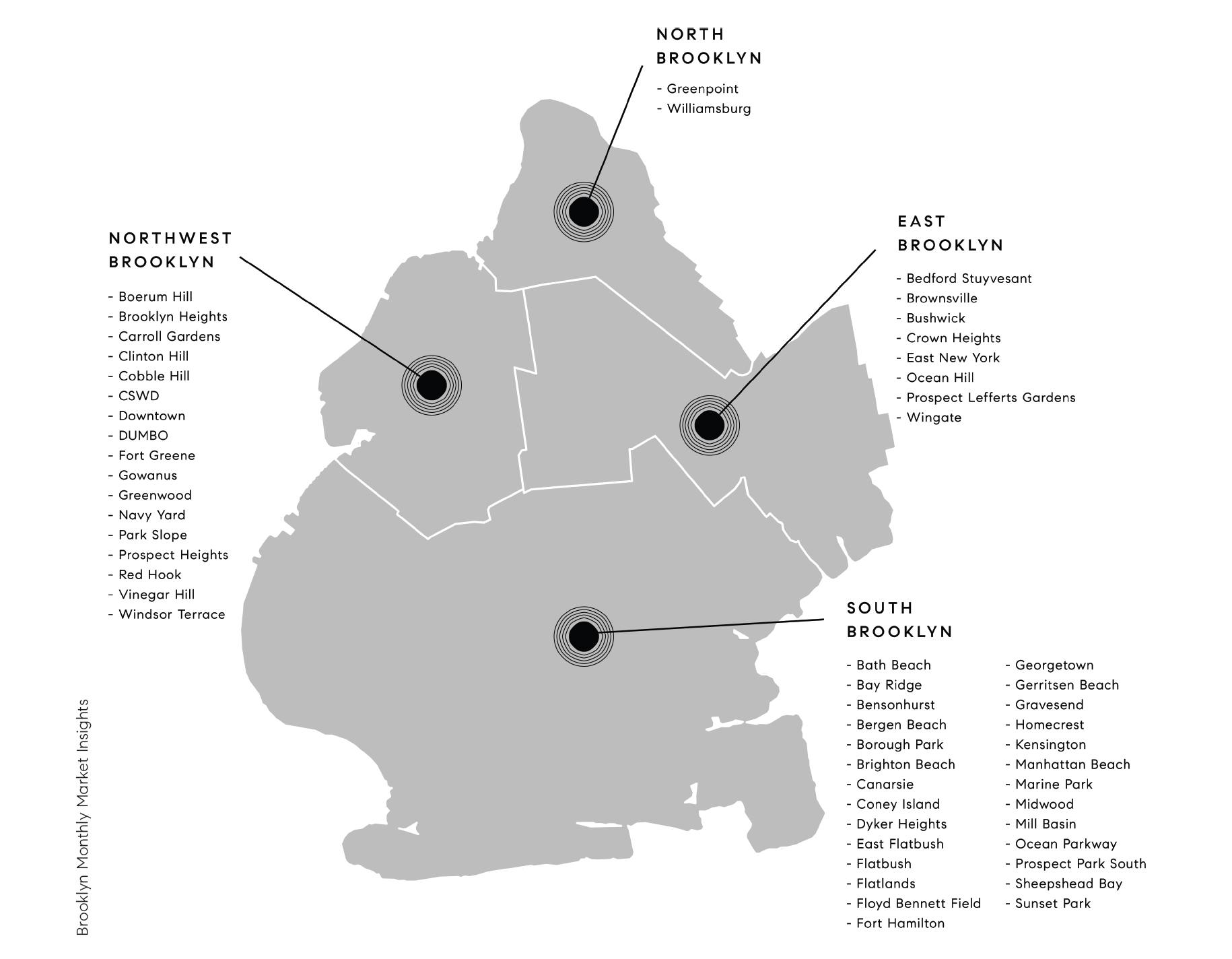

In Brooklyn, prices are still on the rise, although like in Manhattan, days on market has been ticking upward. However, another trend that we had noted earlier this season has become even more pronounced – looking locally rather than borough-wide, in North Brooklyn (Williamsburg & Greenpoint) and North-West Brooklyn (BK Heights, Fort Greene, Park Slope, BoCoCa, etc.), inventory has shrunk faster than contract activity. In September, these sub-markets accounted for 39% of signed contracts vs. 34% of total inventory – last month, they accounted for 42% of signed contracts and just 28% of total inventory. On the other hand, South Brooklyn listings represented 42% of contracts last month but also made up a whopping 54% of total inventory. |

Looking just at BoCoCa (Boerum Hill, Cobble Hill, and Carroll Gardens), demand has outpaced supply dramatically compared to a typical year, and was on par with the incomparable 2021. There were only 155 listings brought to market this season (Labor Day – December 15th) and 95 contracts signed. In 2019, a more typical year, inventory was about the same (157 new listings), but there were almost half the number of contracts signed (50). Despite a higher sales volume in booming 2021, absorption rates were very similar - 258 new listings and 190 contracts signed. So even while overall Brooklyn metrics continue to shift, not all of these trends are consistent across the borough, and many of the figures we've seen this year are actually fairly in-line with pre-Covid figures. While there are certainly fewer buyers out there, with many folks sitting out the current rate environment, low inventory in certain areas has kept the Brooklyn market strong. |

It remains to be seen how the rate environment and market will evolve as we enter 2023, but many believe the worst rate hikes are behind us and mortgage rates have declined and leveled off from October highs. The biggest trend in lending we've seen recently is the rise of the I/O (interest-only) loan. Previously reserved almost exclusively for those with low salaries but high bonuses (like finance people), the I/O loan rates are now even with or lower than amortizing mortgages, especially on smaller loan amounts. Given that most anticipate that rates will go down in the near future (1-5 years), locking in an I/O loan has become a way for buyers to lower their monthly obligations with the expectation of refinancing before the end of the initial period (usually 5, 7, or 10 years). 2022 was certainly a roller-coaster of a year for real estate: the year started off with a bang -- building on 2021's tremendous momentum, Manhattan saw the strongest market it had in years until Fed policy caught up with the market, practically grinding to a halt from Memorial Day onwards. Given that the market dynamics can be almost entirely attributed to monetary policy decisions, many expect this to be a temporary situation, so both buyers and sellers seem to be on the sidelines just waiting to be called into play. When their turn will come remains to be seen, but it is unlikely we'll see a drastic market-wide shift in prices before it course-corrects. |

Blackstone and Starwood are restricting the amount of withdrawals from their non-traded commercial real estate REITS as investors bemoan the volume of debt in the commercial real estate sector and property valuations. |

Investors predict the Fed will cut rates when faced with a slowing economy in 2023, betting the US central bank is far closer to ending its historic monetary tightening campaign than it has signaled. Treasuries futures markets point to the Fed’s benchmark policy rate peaking in May at 4.9% before falling back to 4.4% by the end of 2023. |

According to the National Association of Home Builders, the $4.4 trillion Single-family, built-for-rent (SFR) market is one of the fastest-growing sectors in real estate. SFR homes account for 11% of all single-family home construction, versus a 3% market share that was typical.

(WSJ) |

Peak inflation appears to be behind us as (1) Softening underlying trends in inflation metrics -- prices paid index, manufacturing and services, supply chain indices, and inflation expectations -- all are moving lower; (2) Shelter and rent make up 40% of CPI, but have a lag impact; (3) As global demand for oil and commodities markets has softened, this will trickle down to food prices. ( MARKETWATCH) |

Looking for more? Connect with us for real estate news and market insights. |

Why are mortgage rates lower for a non-conforming (aka jumbo) loan than a conforming loan? First a definition: non-conforming loans are typically where the loan amount is over the limit set by Fannie Mae/Freddy Mac also called "jumbo" loans (currently $647,200, but slated to increase to $715,000 in 2023), where the coop/condo is not warrantable, interest only loans, or where the loan is being held on the bank’s books in order to benefit low-to-moderate income borrowers. You'll notice rates for these loans are often much lower than the same types of loans for conforming loans because they are not guaranteed Fannie Mae/Freddy Mac and are instead held on the bank’s books. This is because: - The bank doesn’t have to pay certain “guarantee-fees” to Fannie Mae and Freddie Mac for ensuring that the agencies will protect the bank if a borrower defaults.

- Non-conforming loan borrowers tend to have higher credit scores, more assets, and are generally lower risk of defaulting than conforming loan borrowers are.

- Non-conforming loans are generally priced to lose money with rates too low to be profitable in hopes of attracting high net worth borrowers to start banking and investing with the bank (which is much more profitable than mortgage lending).

Thank you to Zack Tolmie, mortgage lending officer at Citibank for putting this information together so clearly! |

|

© Compass 2022 ¦ All Rights Reserved by Compass ¦ Made in NYC

Compass is a licensed real estate broker. All material is intended for informational

purposes only and is compiled from sources deemed reliable but is subject to

errors, omissions, changes in price, condition, sale, or withdrawal without

notice. No statement is made as to the accuracy of any description or measurements

(including square footage). This is not intended to solicit property already listed.

No financial or legal advice provided. Equal Housing Opportunity.

All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS.

Photos may be virtually staged or digitally enhanced and may not reflect

actual property conditions.

marketingcenter-newyorkcity-manhattan

|

|

|