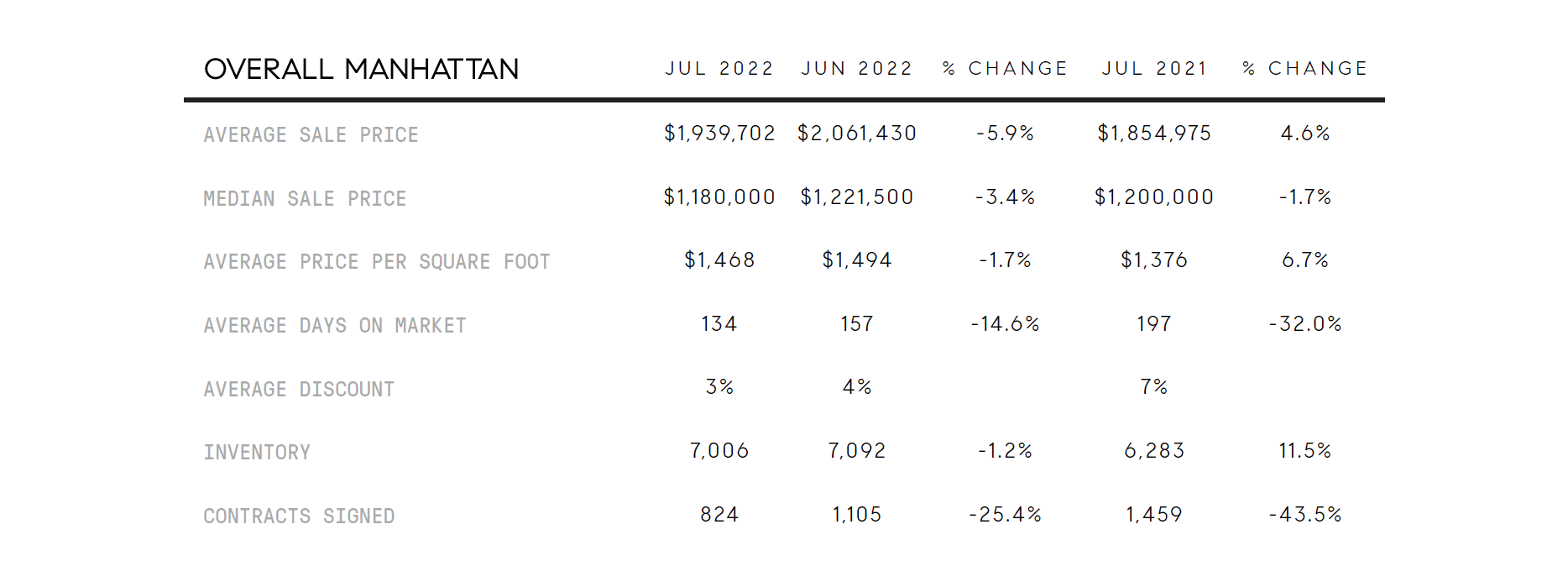

July was a slow month in Manhattan although things seemed to perk up slightly toward the end of the month as both interest rates and the stock market took a turn for the better. Looking at pre-2020 data, the current activity levels seem more indicative of usual seasonal patterns this time of year, and not necessarily the harbinger of a major correction in the NYC market. While Summer 2021 was gangbusters making 2022 look anemic by comparison, contract activity is comparable to July 2019, a strong but ordinary year. There were 774 signed contracts in July 2019 and 824 this July, and the luxury market is significantly stronger this year with luxury contract volume 50% higher than in July 2019 (and only down -15% versus July 2021).

|

While contracts and inventory rates were fairly well-matched across neighborhoods, as usual Downtown performed better, accounting for only 24% of inventory but 28% of contracts signed, and Midtown East lagged with 19% of inventory but only 16% of contracts signed. While median sale prices remained relatively stable, these reflect prices negotiated months prior so the effects of the Summer lull remains to be seen. |

In Brooklyn, average and median sale prices climbed again, although PPSF figures were buoyed by notably strong figures in the townhouse market (+15.6% vs. July of last year). Anecdotally, we are still seeing bidding wars and incredibly low inventory levels with all our townhouse buyers, and inventory levels in the most in-demand areas for all product types has remained quite low. |

So while marketwide contract activity in Brooklyn shows a dramatic decline compared to July of last year, looking closer at the geographic distribution shows that there is a big disparity among regions. Northwest Brooklyn - which includes high-demand neighborhoods like Carroll Gardens, Cobble Hill, Boerum Hill, Park Slope, Prospect Heights & Fort Greene - represented just 22% of inventory but 35% of signed contracts; conversely, South and East Brooklyn made up a combined total of 67% of inventory, but only 55% of contracts. |

While it remains to be seen how the Fall market will play out, as long as interest rates and the stock market stabilize or improve, we might be looking at a return to pre-Covid normalcy and seasonality, especially in Manhattan. While 2021 was anomalous in terms of activity levels and seasonality in NYC, compared to other markets which saw prices skyrocket 30+% above their historical highs, prices in NYC did not wildly deviate from historical highs. As happens almost every Fall, there should be a bump in inventory mid September through October, and we would expect to see price reductions on inventory left over from the Summer. Beyond that, it's hard to make any predictions. |

Mortgage rates fell this week as concerns about a recession outweighed worries about inflation. |

The Manhattan sales market has slowed down. While it may seem dramatic, the data suggests the market is not crashing, but simply returning to normal, seasonal volume. In other words, the slowdown appears to be more of an issue of comparison, and less of a macroeconomic shift. It’s not a crash, it’s a reversion to the mean. (FORBES) |

Nearly 2 million square feet of office space was leased in Midtown in July, a three-fold jump from July 2021 and more than in any month since December 2018. |

Looking for more? Connect with us for real estate news and market insights. |

Make sure to take a peek at our current and upcoming listings below. We’ll be back next month with more real estate news. Until next time! |

|

© Compass 2022 ¦ All Rights Reserved by Compass ¦ Made in NYC

Compass is a licensed real estate broker. All material is intended for informational

purposes only and is compiled from sources deemed reliable but is subject to

errors, omissions, changes in price, condition, sale, or withdrawal without

notice. No statement is made as to the accuracy of any description or measurements

(including square footage). This is not intended to solicit property already listed.

No financial or legal advice provided. Equal Housing Opportunity.

All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS.

Photos may be virtually staged or digitally enhanced and may not reflect

actual property conditions.

marketingcenter-newyorkcity-manhattan

|

|

|