|

|

|

|

The Monica & Mandy Group |

|

WSJ Ranked Among America's Best Teams |

|

Q1 2022 Oerview The market remained heated (probably overheated) in Q1, as our review of home-price appreciation, and supply and demand indicators will illustrate. Also, as of the end of March, mortgage interest rates have jumped 50% in 2022. Because of the time involved in the home-buying process any significant effects of the recent spike won't show up until Q2. However, interest rates are only one factor: Local economic conditions, financial markets, wealth creation, housing affordability, consumer confidence, inflation, migration, the pandemic, war, debt and government policies can all have big market impacts, and they are flashing both positive and negative signals. |

|

What is happening in our market is more complex than we can communicate in the following charts. Reach out to us for more information. We love to discuss the nuances that make our market so unique. |

|

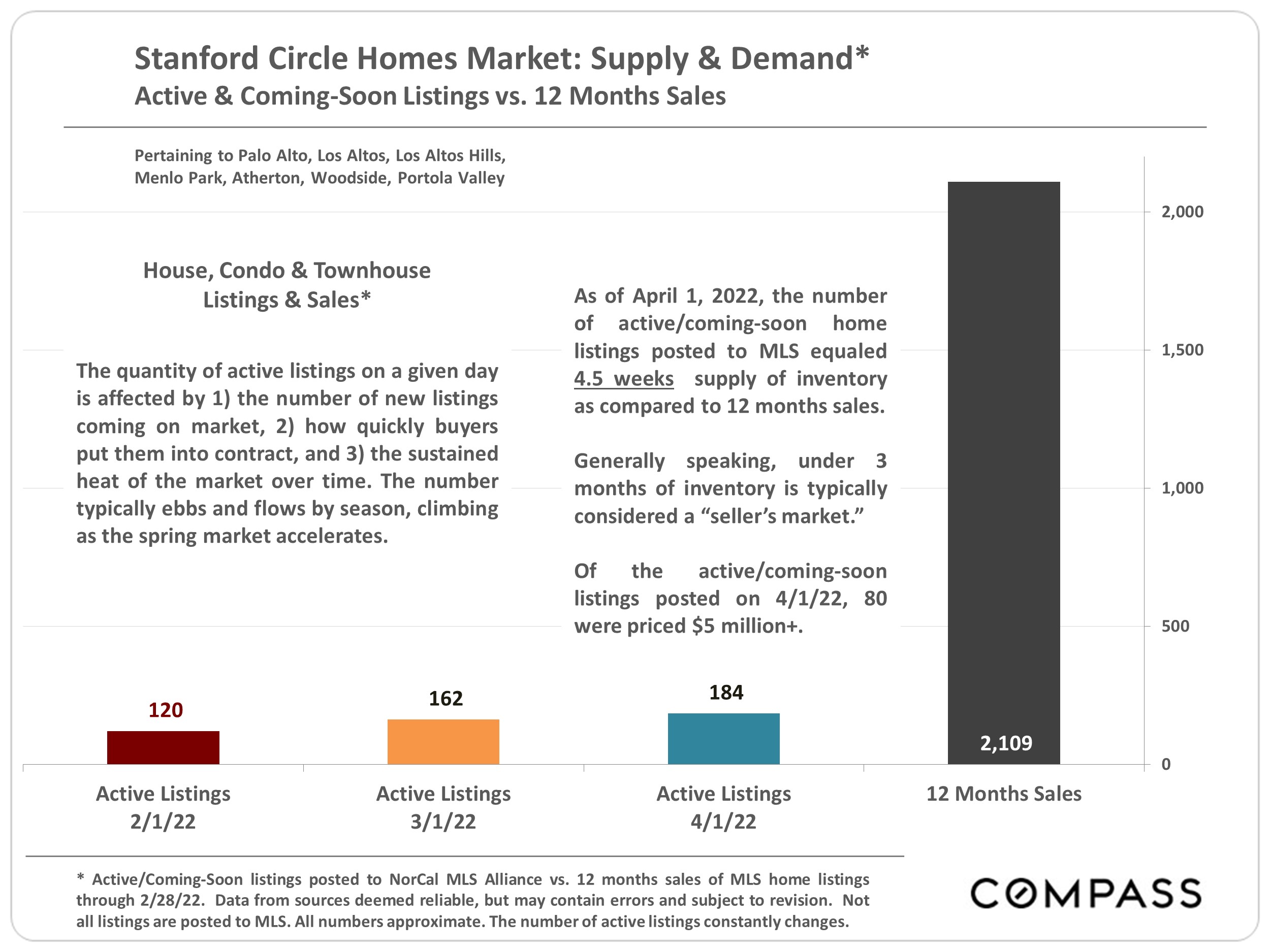

Sales volumes hit multi-year highs in 2021, fed by an increase in new listings. But "inventory" is measured by what is for sale on a given day and the number of active listings can drop if homes are selling extremely quickly. Historically high market activity has been pushing the supply of active listings down to historic lows. |

|

|

An uptick in interest rates combined with higher prices have caused higher monthly payment for most new buyers. |

|

|

Median Home Price Trends In Stanford Circle |

|

|

|

FEATURED PROPERTIES, BUYER NEEDS AND RECENT SALES |

|

We have buyers looking in Atherton, Menlo Park, Palo Alto, Woodside, Portola Valley, and Los Altos Hills in prices ranging from $4M - 15M and are always looking for pre-market opportunities or properties coming soon. If you know of any properties that fit, we would love to hear about them! |

|

|

|

|

|