|

All-cash buyers are common in Manhattan - so the specter of continued interest rate rise, although important, is less likely to be a primary decision-making factor. ...and irregardless of interest rates, overall economic uncertainty has slowed Manhattan sales volume, by fostering a misalignment of buyers' and sellers' expectations. Below please find what I hope will be a helpful market distillation of the tricky, and at times downright confusing real estate market in Manhattan at the moment. It is, as ever, highly segmented by location, price, asset class - and population flows - and there are good current opportunities for both buyers and sellers. As always, please reach out to me if I can answer any questions. |

|

|

|

|

| | |

|

| A Manhattan Real Estate Market: |

|

|

|

|

|

|

Like the U.S. economy, the Manhattan real estate market is in an uncertain period. In February, we learned that the U.S. unemployment rate was at its lowest point since 1969. This week's inflation data confirmed that February remained effectively flat from that of December and January; meanwhile the February jobs' report issued yesterday (3/10/2023) showed a labor market of continued and consistent strength. |

| "...the latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data indicated that a faster tightening is warranted, we'd be prepared to increase the pace of rate hikes." - Jerome H. Powell (3/7/2023) |

| In an economic moment in which high-income New Yorkers are gainfully employed and - despite last year's losses - still benefiting from historic stock market gains, uncertainty in the second half of 2022 resulted in reciprocal inaction on the part of buyers and sellers. Inactivity remained a theme in the first two months of 2023 - and as the weekly volume of new contracts ticks up, nascent hope of a busy spring has arisen alongside enduring uncertainty as to both the speed and potential costs of the path to reduced inflation. |

|

|

|

|

|

|

| Tight inventory yields stable pricing despite lower transaction volume |

| Faced with persistent media warnings of imminent recession in the second half of last year, a significant percentage of potential sellers decided to wait for more advantageous market conditions, and either never listed, or removed their property from the marketplace. The result was a fourth quarter in which fewer Manhattan listings were available than in any 4Q since 2017 - excluding the historic 4Q of 2021. Meanwhile, many buyers waited on the sidelines and watched, anticipating declining prices. This was particularly true in the case of the all-cash purchasers abundant in our market -- who, unmotivated by the threat of rising interest rates, felt empowered to wait for what the media seemed to suggest would be an imminent price correction. Despite the resulting drop in both 4Q '22 closed sales (-24.9% YOY) and new contract volume (-45.2% YOY) -- inventory was up a modest 5.9% year-over-year, with new listings down 27.6% in the same period. Accordingly, quarter-over-quarter pricing metrics were effectively flat in Manhattan at the end of last year, with the median price down 3.5%, the average price up 3.2%, and the average price per square foot up 5.4%. |

|

|

|

|

| "The November figures for resale condo [price per square foot] and resale condo/coop median price show upticks, even with the market slowdown." - UrbanDigs (3/3/2023) |

|

|

|

|

|

|

|

|

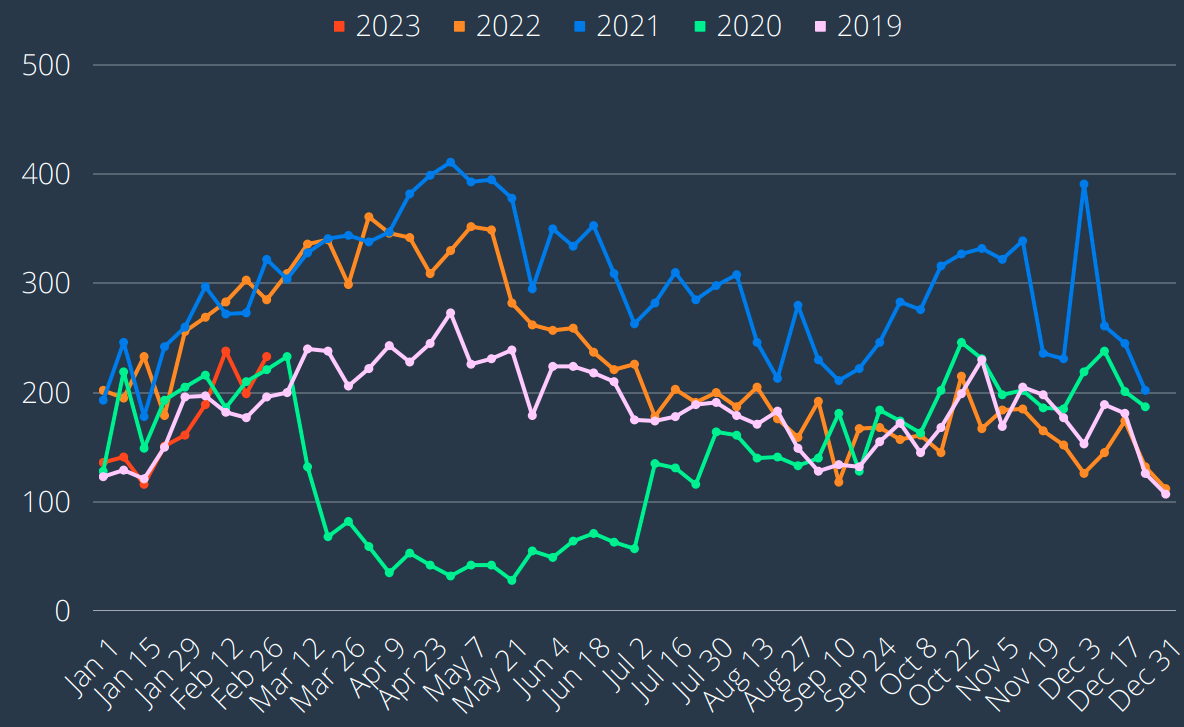

| January and February of 2023: Increase in demand and continuing low inventory |

| | Manhattan Weekend Open House Traffic, Compass Listings: Average number of parties, 11/2022 to present (3/5/2023) |

| Two months into the new year, both open house traffic (see above), and weekly new contract volume (see below) have been trending upwards: "[c]ontracts signed exceeded 200 for the second time this year, which, while below 21/22 levels, is above 2019". (UrbanDigs: 3/3/2023) |

| | Weekly New Signed Contracts: Year-over-year, 2019 to present (UrbanDigs: 3/3/2023) |

| | Inventory: Year-over-year, 2019 to present (UrbanDigs: 3/3/2023) |

| This confluence of lagging inventory (see above) and increased traffic, resulted in supply and demand entering equilibrium for the first time since August 2022 (UrbanDigs, 2/27/23); this trend continued into last week, suggesting a potential move away from what has been a buyers' market, to a more neutral one. In the wake of this week's renewed public commitment to interest rate rise by Chairman Powell, it will be interesting to see how this trend of increased Manhattan activity continues. |

| |

|

|

|

|

|

|

|

|

Office: 646-960-6204 Compass is a licensed real estate broker. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions. |

|

|

|

|

|

|